OPERATIONS MANAGEMENT

CHECK POINT 75: SUPPLY CHAIN AND MATERIALS MANAGEMENT

This Check Point Is Available By Subscription Only,

But You Can Still Check Out The Menu Below. |

|

| |

|

DO I NEED TO KNOW THIS CHECK POINT?

|

| |

OPERATIONS MANAGEMENT

CHECK POINT 75: SUPPLY CHAIN AND MATERIALS MANAGEMENT

Please Select Any Topic In Check Point 75 Below And Click. |

|

| |

|

DO I NEED TO KNOW THIS CHECK POINT?

|

| |

WELCOME TO CHECK POINT 75 |

|

| |

HOW CAN YOU BENEFIT FROM CHECK POINT 75? |

| |

| The main purpose of this check point is to provide you and your management team with detailed information about Supply Chain And Materials Management and how to apply this information to maximize your company's performance. |

| |

| In this check point you will learn: |

| |

• What is supply chain?

• About five steps in the supply chain management strategy decisions.

• About lean operational guidelines for supply chain and materials management.

• About five steps in the implementation of supply management strategies.

• About value analysis and basic value analysis questions.

• About four main functions of materials management.

• About elements and steps in the materials purchasing control procedures.

• How to evaluate various supply sources.

• About two basic material ordering systems.

• About two types of inventory control... and much more. |

| |

LEAN MANAGEMENT GUIDELINES FOR CHECK POINT 75 |

| |

| You and your management team should become familiar with the basic Lean Management principles, guidelines, and tools provided in this program and apply them appropriately to the content of this check point. |

| |

| You and your team should adhere to basic lean management guidelines on a continuous basis: |

| |

| • |

Treat your customers as the most important part of your business. |

| • |

Provide your customers with the best possible value of products and services. |

| • |

Meet your customers' requirements with a positive energy on a timely basis. |

| • |

Provide your customers with consistent and reliable after-sales service. |

| • |

Treat your customers, employees, suppliers, and business associates with genuine respect. |

| • |

Identify your company's operational weaknesses, non-value-added activities, and waste. |

| • |

Implement the process of continuous improvements on organization-wide basis. |

| • |

Eliminate or minimize your company's non-value-added activities and waste. |

| • |

Streamline your company's operational processes and maximize overall flow efficiency. |

| • |

Reduce your company's operational costs in all areas of business activities. |

| • |

Maximize the quality at the source of all operational processes and activities. |

| • |

Ensure regular evaluation of your employees' performance and required level of knowledge.

|

| • |

Implement fair compensation of your employees based on their overall performance.

|

| • |

Motivate your partners and employees to adhere to high ethical standards of behavior. |

| • |

Maximize safety for your customers, employees, suppliers, and business associates. |

| • |

Provide opportunities for a continuous professional growth of partners and employees. |

| • |

Pay attention to "how" positive results are achieved and constantly try to improve them. |

| • |

Cultivate long-term relationships with your customers, suppliers, employees, and business associates. |

|

|

|

1. WHAT IS SUPPLY CHAIN MANAGEMENT? |

|

|

SUPPLY CHAIN MANAGEMENT |

Business owners and operations managers must be fully familiar with various procedures related to supply chain and materials management to ensure cost-effective and profitable performance of the organization.

The prime purpose of Supply Chain Management is to ensure that the organization develops a long-term competitive edge to remain successful in a highly challenging global environment.

The concept of supply chain management has been developed in recent decades and it still undergoes a process of continuous refinement in accordance with the prevailing world class operational guidelines.

A Supply Chain is a sequence of suppliers, warehouses, manufacturing and operational facilities, wholesale distributors, retailers, and ultimate customers - the end-users of products and services.

A supply chain may be different for various companies depending upon their specific nature of business, i.e. manufacturing, merchandising, service, project, or contract as illustrated below. |

SUPPLY CHAIN OVERVIEW |

Manufacturing

Company |

Merchandising Company |

Service

Company |

Project

Or Contract

Company |

Wholesaler

(Distributor) |

Retailer |

1.

Suppliers:

•Distributors

of raw

materials

•Sub-

Contractors |

1.

Suppliers:

•Manufacturers

•Wholesalers |

1.

Suppliers:

•Wholesalers |

1.

Suppliers:

•Wholesalers

•Retailers |

1.

Suppliers:

• Wholesalers

•Retailers |

|

|

|

|

|

2.

Storage

Facility |

2.

Storage

Facility |

2.

Storage

Facility |

2.

Storage

Facility |

2.

Storage

Facility |

|

|

|

|

|

3.

Manufacturing

Company |

3.

Wholesaler |

3.

Retailer |

3.

Service

Company |

3.

Project or

Contract

Company's |

|

|

|

|

|

4.

Storage

Facility |

4.

Storage

Facility |

4.

Storage

Facility |

4.

Storage

Facility |

4.

Storage

Facility |

|

|

|

|

|

5.

Customers:

• Wholesalers

• Distributors |

5.

Customers:

• Retailers |

5.

Customers:

• End-users |

5.

Customers:

•Manufacturers

•Wholesalers

•Retailers

•End-users |

5.

Customers:

•Manufacturers

•Wholesalers

•Retailers

•End-users |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

2. ELEMENTS OF EFFECTIVE SUPPLY CHAIN MANAGEMENT STRATEGY |

|

|

SUPPLY CHAIN MANAGEMENT STRATEGY |

According to Robert L. Evans, every CEO and business owner should be thinking today about the Supply Chain Management Strategy in order to secure the future success of his or her organization.

The Supply Chain Management Strategy, which is closely interrelated with Materials Management, entails formulating a number of important decisions related to the issues of customers, suppliers, sub-contractors, distributors of products, and providers of services. These decisions should include a number of steps illustrated below. (8) |

SUPPLY CHAIN MANAGEMENT STRATEGY DECISIONS

Step 1: Identify The Most Cost-Effective And Optimal Supply Chain For Your Organization.

The supply chain is selected in accordance with the type of company operations, namely: manufacturing, merchandising, service, projects, and contracts.

Step 2: Select A Pool Of Companies With Whom You Want To Connect, Taking Into Account:

- • What your competitors are doing?

- • What your potential partners in the supply chain are doing?

- • What value-adding role will your company plays in the supply chain?

Step 3: Select The Dimensions Across Which You And Your Supply Chain Partners Will Connect And Decide:

- • What information will be shared between partners?

- • Whether product and processes will be jointly designed?

- • What planning and decision making will be shared between partners?

- • How operations could be combined to eliminate redundant assets, reduce costs, and serve customers better?

- • How the financial terms will be arranged between partners?

Step 4: Select The Organizational Form Your Supply Chain Will Take And Decide Whether It Should Be:

- • Continuous business relationship of buying and selling products and services.

- • Merger with a supply chain partner.

- • Acquisition of a supply chain partner.

Step 5: Finalize Your Selection Of Supply Chain Partners.

Your selection must be based on the most economically viable long-term mutually beneficial association. |

|

© Robert L Evans, What CEO's Should Know About Supply Chain Strategy. Adapted from Supply Chain Management Review Global Supplement, Spring 1999, pp. 27-28. |

ADDITIONAL INFORMATION ONLINE |

|

You can obtain additional information about Supply Chain Management online:

|

|

|

3. LEAN OPERATIONAL GUIDELINES FOR SUPPLY CHAIN MANAGEMENT |

|

|

IMPORTANCE OF LEAN OPERATIONAL GUIDELINES |

In order to remain successful in the highly competitive business environment, it is essential that you and your management team become familiar with the existing Lean Operational Guidelines related to supply chain and materials management. These guidelines may include several elements outlined below. |

LEAN OPERATIONAL GUIDELINES

FOR SUPPLY CHAIN AND MATERIALS MANAGEMENT

Materials Purchasing:

- • Identify and pre-select a minimal number of highly reliable suppliers of products and services required on a regular basis.

- • Arrange purchases of larger quantities of materials and services at most competitive prices during one fiscal year period to secure maximum quantity discounts and most favorable payment terms.

- • Arrange for partial deliveries of products and services to meet current work load levels while maintaining minimal inventory levels.

- • Maximize the cooperation with all regular suppliers of materials and services and sub- contractors.

- • Minimize the lead delivery times for products and services.

- • Maximize the overall manufacturing cost-effectiveness by out-sourcing or sub-contracting selected components for manufacture and/or assembly, and other related services.

Materials Control:

- • Maximize the use of computerized inventory control systems.

- • Maintain updated information related to current inventory levels.

- • Maintain updated information related to material and services cost control.

- • Implement the use of standard containers for material handling throughout the facility.

- • Maximize the use of light signals for material replenishment requirements at specific work stations.

- • Implement the use of "Kanban" cards.

Materials Storage:

- • Minimize the storage space requirements for raw materials, work-in-process, finished goods, and tooling by reducing the inventory level requirements, and utilizing the height of existing storage facilities.

- • Maximize the use of material handling and lifting equipment and conveyor lines to distribute materials from the stores to work stations.

- • De-centralize material and tooling storage and locate same as close as possible to relevant work stations to minimize the waste in travel, time, and labor.

- • Prepare tooling kits for special tasks, jobs, or operations.

- • Maximize the perimeter access for receiving and shipping materials.

- • Maximize the issue of materials for several production orders.

Materials Dispatch And Distribution:

- • Plan dispatch of finished products to customers in advance to take advantage of most cost-effective routing and available transportation space.

- • Maintain effective cost control of materials and services dispatch and distribution to customers.

- • Maintain effective operational control over the existing transport facilities.

|

Lean Management is discussed in detail in Tutorial 1. |

|

|

|

4. IMPLEMENTATION OF SUPPLY CHAIN MANAGEMENT STRATEGIES |

|

|

SUPPLY CHAIN MANAGEMENT STRATEGIES |

The process of Supply Chain Management Strategies implementation entails a number of important steps which are outlined below. |

IMPLEMENTATION OF SUPPLY CHAIN MANAGEMENT STRATEGIES

Step 1: Evaluate The Effectiveness Of Internal Material Management Within The Organization Through Value Analysis.

Step 2: Identify And Evaluate Sources Of Materials And Services Supply Through Vendor Analysis.

Step 3: Develop Strategic Alliances With Selected Suppliers Of Materials And Services.

Step 4: Implement Cost-Effective Methods Of Planning And Control Related To Material Purchasing, Receiving, Control, Storage, And Dispatch.

Step 5: Establish Sound Relations With Customers To Ensure Continuous Stability And Growth Of The Supply Chain Management Process. |

|

|

5. VALUE ANALYSIS |

|

|

WHAT IS VALUE ANALYSIS? |

In order to achieve success by implementing an effective supply chain management strategy, it is essential to identify inefficiencies within the organization and eliminate or minimize them in a planned and systematic manner. This entails evaluating all departments and work centers within your organization which are related to purchasing, receiving, control, storage, and distribution of materials.

Such evaluation entails a detailed Value Analysis related to the several functions and activities outlined below. |

AREAS WHICH REQUIRE VALUE ANALYSIS |

1. |

Purchasing of products and services. |

2. |

Receiving of materials. |

3. |

Storage of materials. |

4. |

Product design. |

5. |

Product manufacturing. |

6. |

Product dispatch and distribution. |

7. |

Accounting and data processing control. |

|

| |

VALUE ANALYSIS = VALUE ENGINEERING |

Value Analysis is often called Value Engineering (VE). This method is designed to maximize the value of products, services, projects, and processes through a systematic evaluation of their functions and costs. Value is defined as a ratio of function to cost and it can be improved by increasing the scope of the function or decreasing the cost. Value engineering was originally termed value analysis and developed by Lawrence D. Miles during 1940's in U.S. |

The basic Value Analysis Questions, outlined below, represent an integral part of the lean operational guidelines related to continuous improvement of products and services. |

BASIC VALUE ANALYSIS QUESTIONS |

1. |

Is a particular operation or activity really essential and does it increase the final value of a particular product or service? |

2. |

Can the product or process be purchased in a more cost-effective manner? |

3. |

Can the lead time for purchased materials and components be reduced? |

4. |

Is a particular component really necessary for the final assembly? |

5. |

Can materials and components be stored in a more cost-effective manner? |

6. |

Can finished products be distributed in a more cost-effective manner? |

7. |

Do employees have suggestions for materials management improvements? |

8. |

Can the product dispatch and distribution be accomplished in a more cost-effective manner? |

|

| |

VALUE ANALYSIS IN LEAN ENVIRONMENT |

You and your management team should also become familiar with various elements of Lean Management which include the following: |

|

Lean Management is discussed in detail in Tutorial 1. |

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

6. MATERIALS MANAGEMENT |

|

|

MATERIALS MANAGEMENT |

A broad range of material-related activities, which represent an integral part of the supply chain management, is constantly conducted within a company. All such activities fall into the scope of Materials Management which is defined as:

"The coordinated function responsible to plan for, acquire, store, move, control and dispatch materials and final products to optimize usage of facilities, employees, capital funds, and to provide customer service in line with corporate goals."(9)

Materials management is becoming increasingly important in manufacturing as well as non-manufacturing organizations. The various activities included in this function are illustrated below. |

MATERIALS MANAGEMENT FUNCTIONS |

|

|

|

|

Materials

Purchasing |

Materials

Receiving

|

Inventory

Control

|

Dispatch And Distribution

Of Finished

Products

|

|

|

|

|

7. MATERIALS PURCHASING |

|

|

MATERIALS PURCHASING |

Materials Purchasing can be defined as: "the responsibility to buy materials of the right quality, in the right quantity, at the right time, at the right price from the right source with delivery at the right place". (10)

Materials purchasing involves a number of activities which have been summarized by James B. Dilworth and outlined below. (11) |

MATERIALS PURCHASING ACTIVITIES |

1. |

To locate, evaluate and develop sources of materials, supplies and services that the company needs. |

2. |

To ensure good working relations with these sources in such matters as quality, delivery, payments, and exchanges or returns. |

3. |

To seek out new materials and products and new sources of better products and materials so that they can be evaluated for possible use by the company. |

4. |

To purchase wisely all items that the company needs at the best possible price consistent with quality requirements and to handle the necessary negotiations to carry out this activity. The best value does not always represent the lowest initial cost, so products should also be evaluated for their expected lifetime, serviceability, and maintenance cost. |

5. |

To initiate, if necessary, and to cooperate in cost-reduction programs, value analysis, make-or-buy studies, market analyses, and long-range planning. Purchasing should keep abreast of trends and projections in prices and availability of the inputs that a company must have. |

6. |

To work on maintaining an effective communication linkage between departments within the company and between the company and its suppliers or potential suppliers. |

|

The purchases and disbursements control process can be maintained manually or by using a specific Accounting Software Program as discussed in detail in Tutorial 3. |

POPULAR ACCOUNTING SOFTWARE PROGRAMS |

There are several excellent accounting software programs available to small business owners at present. Some of the popular accounting software packages are: |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

8. STEPS IN MATERIALS PURCHASING PROCEDURE |

|

|

Materials Purchasing Procedure entails a number of steps which are summarized below. |

MATERIALS PURCHASING PROCEDURE

Step 1: Recognize The Need For Materials.

Step 2: Define The Materials Requirements.

Step 3: Identify Possible Sources Of Supply.

Step 4: Obtain And Confirm Prices And Delivery Dates.

Step 5: Select The Most Appropriate Supplier And Place A Purchase Order.

Step 6: Follow-Up And Expedite The Purchase Order.

Step 7: Verify The Supplier's Invoice Against The Order.

Step 8: Ensure That All Discrepancies Are Corrected. |

|

|

9. ELEMENTS OF PURCHASING CONTROL |

|

|

PURCHASING CONTROL |

Control of purchases and disbursements represents an integral part of materials purchasing. This process can be completed manually or by using an purchasing software program. |

Purchasing Control is discussed in detail in Tutorial 3. This procedure includes a number of elements illustrated below. |

CONTROL OF PURCHASES AND DISBURSEMENTS

Step 1: Complete A Purchase Requisition.

Purchase originator completes a purchase requisition specifying the required goods.

Step 2: Authorize The Purchase Requisition.

Head of the department authorizes the purchase requisition.

Step 3: Place A Purchase Order.

Buyer places a purchase order with a suitable supplier for the supply of goods.

Step 4: Accept The Delivery Of Goods.

The delivery of goods from supplier is received, inspected, and accepted.

Step 5: Issue Goods.

Goods are issued to the purchase requisition originator.

Step 6: Prepare Documentation.

All supporting documentation related to the delivery of goods is passed to the financial department for payment processing to the supplier. |

|

|

|

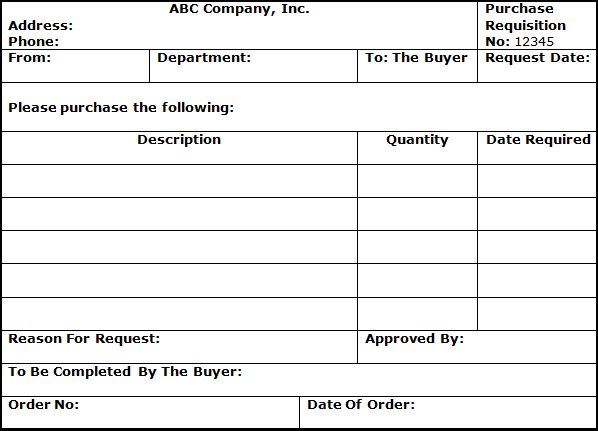

10. PURCHASE REQUISITION |

|

|

PURCHASE REQUISITION |

The Purchasing Control usually begins with an appropriate Purchase Requisition specifying a detailed description, quantity of required items, and delivery dates of required materials or services. Each Purchase Requisition is completed in duplicate by a purchase requisition originator in accordance with specific operational requirements outlined below. |

PURCHASE REQUISITION PROCEDURE |

1. |

The first copy of the purchase requisition is sent to the head of the department for approval to ensure effective control over purchasing activities. |

2. |

The second copy is kept by the purchase requisition originator. |

|

Upon its approval, the purchase requisition is forwarded to the company's Buyer and is used as a detailed purchasing instruction. |

In a computerized purchasing system, the data describing each purchase requisition is entered at the start of the purchasing cycle. Subsequently, this information is processed and distributed to the head of the department for approval. |

|

|

11. SMALL BUSINESS EXAMPLE

PURCHASE REQUISITION |

|

|

| |

PURCHASE REQUISITION |

|

|

|

12. THE SUPPLY SOURCES EVALUATION |

|

|

THE SUPPLY SOURCES EVALUATION |

The Supply Sources Evaluation is an essential part of the supply chain management strategy implementation. The supply sources evaluation, or Vendor Analysis, entails the consideration of several factors related to the existing and potential suppliers of products and services as outlined below. |

VENDOR ANALYSIS

Quality And Reliability:

- • How reliable are the products and services provided by the supplier?

- • What kind of internal quality control procedures does the supplier have?

- • Can supplier produce documentation relevant to quality control?

Price And Discounts:

- • How does the supplier's price compare with other suppliers taking into consideration the entire package?

- • Is the supplier willing to negotiate the price and offer quantity discounts based on a long- term commitment to buy?

- • Is the supplier willing to participate in a joint effort in order to reduce the ultimate price?

After-Sales Service:

- • Does the supplier offer specific guarantees related to the after-sales service?

- • Is the supplier prepared to offer additional assurances related to efficient resolution of problems which may arise after the product or service has been purchased?

Lead Time And Timely Delivery:

- • Does the supplier offer product or service delivery at acceptable lead times?

- • Is the supplier prepared to accelerate the lead time and provide smaller quantities of products or services on a more frequent basis?

- • Does the supplier keep promises related to the delivery dates of products and services?

Supplier's Location:

- • Is the supplier located in a relatively close proximity to the buyer?

- • Does the distance between the supplier and the buyer present a negative factor?

Supplier's Inventory Policy:

- • Does the supplier keep additional products in inventory in case of emergency orders by the buyer?

- • Does the supplier keep additional spare parts in case of emergency equipment breakdowns?

Supplier's Flexibility:

- • How flexible is the supplier in handling fluctuation in quantities of ordered goods or services?

- • Is the supplier willing to redesign certain products to meet the buyer's needs?

Supplier's Reputation And Financial Stability:

- • Is the supplier a well-established company which has a name in the marketplace?

- • Has the supplier been in financial difficulties in recent years?

- • Does the supplier have a good reputation among other customers?

Supplier's Other Accounts:

- • Is the supplier heavily dependent upon a small number of customers or has a wide customer base?

- • Does the supplier offer a preferential treatment of a few selected customers at the expense of other customers, or provide fairly equal treatment to all customers?

|

|

ADDITIONAL INFORMATION ONLINE |

|

|

|

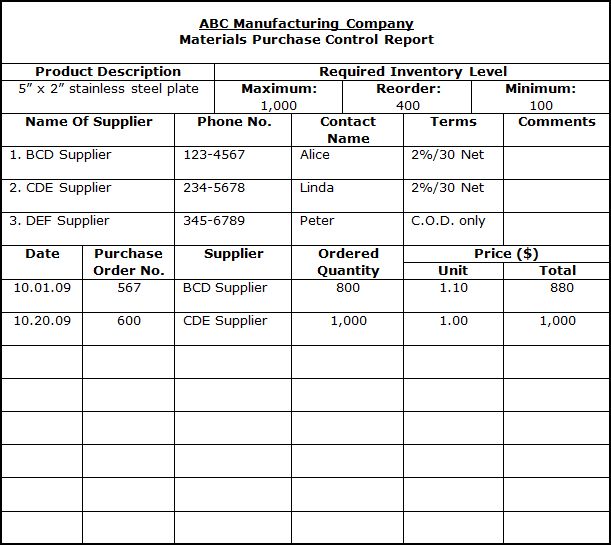

13. MATERIALS PURCHASE CONTROL REPORT |

|

|

MATERIALS PURCHASE CONTROL REPORT |

It is the responsibility of the company's buyer to develop and maintain an effective purchase control system and to prepare a separate Materials Purchase Control Report for every frequently-purchased item.

Such a report may be prepared through a manual or computerized system. The prime purpose of this report is to provide an updated record of inventory requirements and a purchasing history of a specific item. A typical Materials Purchase Control Report is presented below. |

MATERIAL PURCHASING SOFTWARE PROGRAMS |

Material purchasing and control can also be accomplished with several accounting software programs. Accounting Software Program as discussed in detail in Tutorial 3.

There are several excellent accounting software programs available to small business owners at present. Some of the popular accounting software packages are: |

|

|

|

14. SMALL BUSINESS EXAMPLE

MATERIALS PURCHASE CONTROL REPORT |

|

|

MATERIALS PURCHASE CONTROL REPORT |

|

|

|

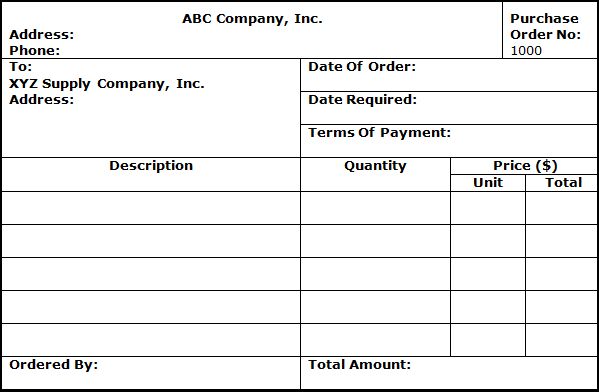

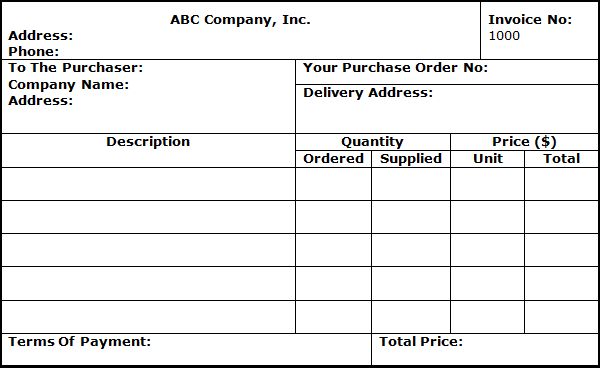

15. PURCHASE ORDER |

|

|

PURCHASE ORDER |

After selecting possible sources of materials or services supply, the Buyer must confirm the prices and delivery dates in order to meet operational requirements. When the final selection is made, a Purchase Order should be prepared and sent to the most suitable Supplier, containing specific order details outlined below. |

PURCHASE ORDER DETAILS |

1. |

Description of goods or services. |

2. |

Quantity required. |

3. |

Unit cost, total price, terms of payment, and possible discounts. |

4. |

Delivery date required and other shipping instructions. |

|

Purchase orders can be prepared manually or generated by a computer and are usually made out in triplicate. |

PURCHASE ORDER DOCUMENTATION |

1. |

The original is sent to the supplier by regular mail, fax, or e-mail. |

2. |

The second copy and a copy of the requisition are sent to the storekeeper, manually or through a computer terminal. |

3. |

The last copy remains in the file in the buyer's office. |

|

| |

CONFIRMATION OF A PURCHASE ORDER |

Relevant details pertaining to each purchase order must be confirmed by the supplier and clearly marked by the buyer on the remaining copy of the purchase order.

Some companies send An Acknowledgment Copy of the purchase order to the supplier. On this copy the supplier confirms the acceptance of the purchase order, specifies the promised delivery date, and returns the completed copy to the buyer. |

|

|

16. SMALL BUSINESS EXAMPLE

PURCHASE ORDER |

|

|

PURCHASE ORDER |

|

|

|

17. PURCHASING CONTROL PROCEDURES |

|

|

PURCHASING CONTROL PROCEDURES |

The buyer enters each Purchase Order into the "Order Follow-Up" File until actual delivery takes place. The follow-up of each order is essential to ensure that all promised delivery dates are met by suppliers.

When materials are finally delivered they should be received in the company's stores. The storekeeper has been already notified about pending delivery by means of copies of the requisition and the purchase order issued to him earlier. These documents are kept by the storekeeper in the "Pending Delivery" File until the actual arrival of materials. |

|

|

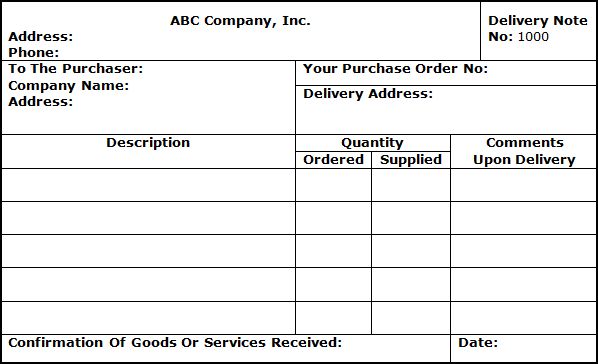

18. THE SUPPLIER'S DELIVERY NOTE AND INVOICE |

|

|

THE SUPPLIER'S DELIVERY NOTE AND INVOICE |

Upon receiving the purchase order, the supplier is expected to deliver the goods or to render services strictly in accordance with the details specified therein. Such a delivery should be accompanied by the supplier's Delivery Note or Bill Of Lading (in duplicate), or Invoice, or both.

The delivery note, illustrated below, contains a detailed description and an indication of the quantity of goods or services. The invoice, in addition, specifies the price and terms of payment as illustrated below. |

|

|

19. SMALL BUSINESS EXAMPLE

DELIVERY NOTE |

|

|

DELIVERY NOTE |

|

|

|

20. SMALL BUSINESS EXAMPLE

INVOICE |

|

|

INVOICE |

|

|

|

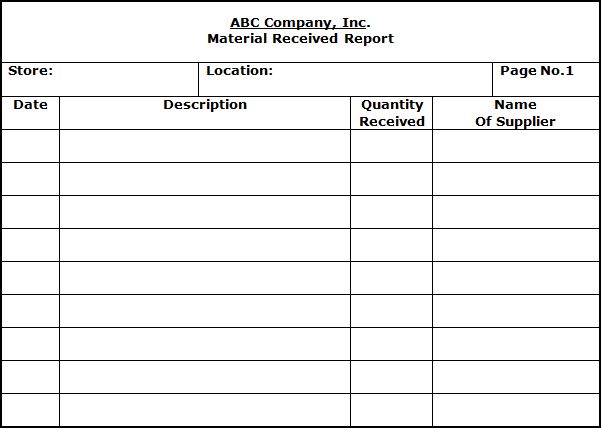

21. MATERIALS RECEIVED REPORT |

|

|

MATERIALS RECEIVED REPORT |

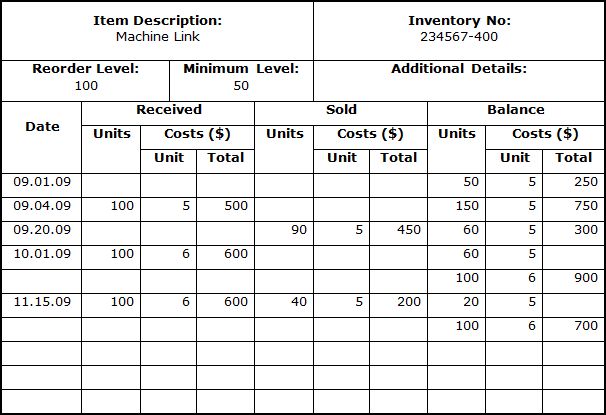

Upon their Delivery, all materials must be properly inspected and the supplier's delivery note and invoice verified against the original purchase order.

It is essential to ensure that there are no Discrepancies in the documentation and that the delivery is found in good order. If any materials are rejected by the Storekeeper, they must be returned to the supplier and replaced as soon as possible.

Both copies of the Delivery Note must be signed by the storekeeper to confirm complete or partial acceptance of the delivery. A signed delivery note, an invoice (if supplied), copies of the purchase requisition, and the purchase order should be sent to the financial department for further processing and payment of accounts.

Sometimes suppliers send the Invoice directly to the financial department after the delivery takes place. Finally, a record should be entered into the Materials Received Report, manually or through a computer, giving the details of the delivery. This record provides entry information for inventory control purposes and is illustrated below. |

|

|

22. SMALL BUSINESS EXAMPLE

MATERIALS RECEIVED REPORT |

|

|

MATERIAL RECEIVED REPORT |

|

|

|

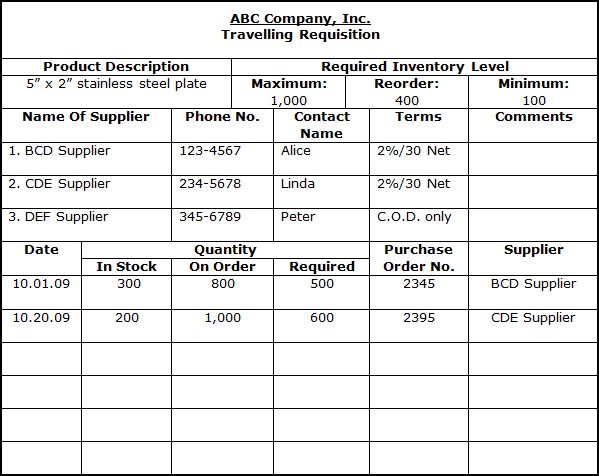

23. AUTOMATION OF THE PURCHASING PROCEDURE |

|

|

AUTOMATION OF THE PURCHASING PROCEDURE |

Depending on the company's size and subsequent requirements for materials and services, the Purchasing Procedure can be carried out manually or through a computerized software program.

A manual procedure is frequently used by smaller organizations where the volume of paperwork is relatively small. When the company grows, however, and places more and more Purchase Orders with various suppliers, the volume of the paperwork may increase dramatically.

This often necessitates automation of the purchasing procedure and reduction of the number of forms. At this stage a Traveling Requisition for all frequently purchased items should be introduced. |

TRAVELING REQUISITION |

1. |

A typical traveling requisition can be prepared manually or generated by a computer. |

2. |

The traveling requisition lists in permanent blocks, all descriptive information about the item requested, the approved suppliers, their phone numbers, and past pricing information. |

3. |

The traveling requisition is kept in the work center where a particular item is being used, and lists the current quantity of the item in stock, the desired quantity, and the date. |

4. |

This form is then sent to the company's buyer and serves as instruction for a purchase order. Thereafter, the traveling requisition is returned to the requisitioning work center and is kept there for future use. |

|

The traveling requisition saves time and helps reduce the volume of paperwork in companies that use a manual system. When the company continues to grow, management may decide to computerize the purchasing procedure and incorporate it with other functional activities. |

|

|

24. SMALL BUSINESS EXAMPLE

TRAVELING REQUISITION |

|

|

TRAVELING REQUISITION |

|

|

|

25. INVENTORY CONTROL |

|

|

INVENTORY CONTROL |

|

Business owners and operations managers must be fully familiar with the materials control, or inventory control procedures, which represent one of the critical elements of operations management.

Inventory Control is particularly important since many companies are compelled to keep a broad range of costly inventories in order to meet their operational requirements. The classification of inventories in various types of companies, discussed in detail in Tutorial 3, is summarized below.

Depending on the company's size and subsequent requirements for materials and services, the inventory control can be carried out manually or through a computerized software program. |

CLASSIFICATION OF INVENTORY |

|

|

|

|

|

Service

Company |

|

Merchandising

Company |

|

Manufacturing

Company |

A service company usually does not carry inventory except for some consumable items, whenever required, such as:

| • |

Spare Parts. |

| • |

Consumable Supplies. |

|

|

A merchandising company carries inventory for resale known as Merchandise Inventory. |

|

A manufacturing company carries three types of inventory:

| • |

Direct Materials Inventory. |

| • |

Work-In-Process Inventory. |

| • |

Finished Goods Inventory. |

|

|

|

Inventory Management is discussed in detail in Tutorial 3. |

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

26. INVENTORY COSTS |

|

|

INVENTORY COSTS |

Inventory is important for several reasons. It enables a company to meet fluctuating customer requirements, to stabilize the utilization of operational capacity and human resources, and to minimize the effect of material shortages. However, inventory is often associated with substantial costs outlined below. |

TYPICAL INVENTORY COSTS |

1. |

Cost Of Goods Ordered.

This includes the actual investment in goods purchased by the company. |

2. |

Setup Cost.

This includes the overall administrative overhead, which relates to the purchasing function within the company. |

3. |

Goods Holding Cost.

This includes the interest payable on investment that has been used to purchase the goods. |

4. |

Storage Cost.

This includes the overall costs of keeping and handling goods in the stores. |

5. |

Stock Shortage Cost.

This includes all losses which may occur as a result of inventory shortage, like loss of sale, idle machine, and labor time. |

|

|

|

27. TWO BASIC MATERIAL ORDERING SYSTEMS |

|

|

IMPORTANCE OF TIMING IN EFFICIENT INVENTORY PLANNING |

An integral part of efficient Inventory Planning And Control entails determination of correct timing for ordering correct quantities of certain type of inventories.

Various types of Material Ordering Systems deal with these important questions. Some systems are based on a dependent demand for inventory, such as Material Requirements Planning (MRP) , while others are based on an independent demand for inventory. The basic difference between the two systems is illustrated below. |

TWO BASIC MATERIAL ORDERING SYSTEMS |

|

|

|

Dependent

Demand For Inventory |

|

Independent

Demand For Inventory |

| The materials ordering system is "driven" by specific manufacturing requirements, like Materials Requirements Planning. (MRP). |

|

The materials ordering system is based on a Pre-Determined Reorder Level, Economic Order Quantity, Reorder Point System, or Periodic Review System. |

|

|

Materials ordering based on a dependent demand for inventory, i.e. Material Requirements Planning, is discussed in detail in Tutorial 4. The second type of materials ordering is based on an independent demand for inventory and includes two systems illustrated below. |

TWO SYSTEMS OF CONTROL BASED ON

THE INDEPENDENT DEMAND FOR INVENTORY |

|

|

|

Reorder Point

System |

|

Periodic Review

System |

|

|

|

|

28. REORDER POINT SYSTEM |

|

|

REORDER POINT SYSTEM |

A Reorder Point System entails a pre-determination of the minimum inventory level for every item kept in stock.

Whenever the inventory on hand reaches the minimum level, or Reorder Point, a purchase order must be placed for a pre-specified quantity of goods.

The Reorder Point is established so that the inventory on hand will be sufficient to meet the production demand during the Lead Time, the time between placement of a purchase order and receipt of materials. The Reorder Point System is clarified below. |

REORDER POINT SYSTEM ILLUSTRATION |

|

|

|

29. ECONOMIC ORDER QUANTITY MODEL |

|

|

ECONOMIC ORDER QUANTITY MODEL |

The Lead Time for different materials varies, depending upon the particular suppliers. It is necessary, therefore, to establish the lead time for every inventory item well in advance in order to determine the Minimum Inventory Level.

The pre-specified quantity of inventory to be purchased at the reorder point is generally based on the Economic Order Quantity (EOQ) Model. The basic assumptions underlying the EOQ Model are outlined below. |

ECONOMIC ORDER QUANTITY MODEL ASSUMPTIONS |

1. |

Constant demand for products. |

2. |

The lead time is known well in advance. |

3. |

Every order arrives in one complete delivery without partial order deliveries or back-orders. |

4. |

The cost of placing and receiving an order remains constant irrespective of the order size. |

5. |

The cost per item remains constant irrespective of the order size. |

6. |

The cost of holding an inventory item remains constant irrespective of the number of items held in stock. |

|

| |

ECONOMIC ORDER QUANTITY FORMULA |

The EOQ Model does not provide a perfect answer since the above mentioned assumptions are seldom realized in the actual business environment. Under suitable conditions, however, this model may provide a starting point for determining the Economic Order Quantity.

The EOQ Formula is presented below. |

|

KEY: |

N |

Number of units used during one year. |

S |

Average order-related cost (i.e. the cost of preparing the order, driver, transportation, and other relevant administrative expenses). |

H |

The cost of holding a unit of inventory during one year. |

|

|

|

30. SMALL BUSINESS EXAMPLE

APPLICATION OF ECONOMIC ORDER QUANTITY FORMULA |

|

|

APPLICATION OF ECONOMIC ORDER QUANTITY FORMULA |

|

An application of the EOQ Formula is illustrated in the following example.

A company is using 10,000 units of Product A during one year, whereby:

- • The average order-related cost is $15.

- • The cost of holding a product unit during one year is $5, since an item costs $50 and the annual interest rate is 10%.

Thus, the Economic Order Quantity can be computed as follows: |

|

|

|

31. PERIODIC REVIEW SYSTEM |

|

|

PERIODIC REVIEW SYSTEM |

A Periodic Review System, as its name implies, entails reviewing the inventory level at equal intervals and maintaining it at pre-determined levels by ordering additional quantities of materials. |

MAXIMUM LEVEL OF INVENTORY |

A Maximum Level Of Inventory needs to be established for each stock item to secure correct reordering of required materials. The quantity of materials that need to be reordered can be determined as follows:

Reorder Quantity = A - B - C + D |

KEY: |

A |

Maximum level of inventory. |

B |

Inventory "on-hand", i.e. available in stock. |

C |

Inventory "on-order", i.e. materials ordered but not yet received. |

D |

Expected demand of inventory during the lead period. |

|

|

|

32. TWO TYPES OF INVENTORY CONTROL |

|

|

INVENTORY CONTROL SYSTEMS |

Depending upon the company's size, nature of operations, and range of materials and products, the Inventory Control System can be maintained on a manual basis or in a computerized form.

The two basic Inventory Control Systems, which can be used by the company, are described in detail in Tutorial 3 and are illustrated below.

A Perpetual Inventory Control System is commonly used by small and medium-sized companies. Under this system, the following information becomes available for each inventory item as illustrated below. |

TWO TYPES OF INVENTORY CONTROL |

|

|

|

Periodic Inventory System |

|

Perpetual Inventory System |

| This system is based on counting inventory on a periodic basis, possibly once every six or twelve months. Under this system, no detailed record of inventory status is kept during the year. |

|

This system entails recording every transaction pertaining to movement of inventory on a continuous basis. Under this system, every purchase, entry, withdrawal, and sale of inventory is recorded in a Perpetual Inventory Record Card, illustrated below. |

|

|

A PERPETUAL INVENTORY CONTROL SYSTEM |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

33. SMALL BUSINESS EXAMPLE

PERPETUAL INVENTORY RECORD CARD |

|

|

PERPETUAL INVENTORY RECORD CARD |

|

|

|

34. ABC INVENTORY ANALYSIS |

|

|

ABC INVENTORY ANALYSIS |

Many companies keep fluctuating quantities of different types of inventories in their stores on a regular basis. Business owners and operations managers constantly need to know which types of inventories are in higher demand and which ones are in lower demand. Moreover, it is necessary to determine values of various types of inventories, since some of them may require a substantial investment of company resources.

Obviously, when the company’s resources are tied up in slow-moving and costly inventories, this represents a highly undesirable situation which should be rectified as soon as possible. For this reason, it is essential to have a meaningful evaluation of all inventories within the company and to classify these inventories in such a way that will enable the company to be cost-effective and profitable.

One popular method of inventory classification and evaluation frequently used by companies of all sizes is called ABC Inventory Classification or ABC Inventory Analysis. This method was introduced by H. Ford Dickie several decades ago and it still provides a useful way of classification and valuation of inventories. According to this method, all inventories should be classified into one of three categories based on annual dollar volume.

The determination of Annual Dollar Volume entails identification of demand for specific inventory, which is driven by the company’s customers, based on annual volume and the inventory unit cost. Based on ABC Inventory Analysis, all inventories can be classified into three distinctive categories, namely Class A, Class B, and Class C, as illustrated below. |

THREE CATEGORIES OF ABC INVENTORY ANALYSIS |

|

|

|

|

|

Class A:

High Value Items |

|

Class B:

Medium Value Items |

|

Class C:

Low Value Items |

Approximately 20% of all inventory items may account for about 70% of the total inventory value. |

|

Approximately 30% of all inventory items may account for about 20% of the total inventory value. |

|

Approximately 50% of all inventory items may account for about 10% of the total inventory value. |

|

|

ABC INVENTORY ANALYSIS IMPLEMENTATION |

ABC Inventory Analysis can be implemented by using an ABC Inventory Analysis Worksheet, illustrated below. All inventory items should be pre-classified based on their Annual Dollar Volume, which can be determined as follows:

Annual Dollar Volume = Annual Volume (In Units) x Unit Cost

The information about each inventory item needs to be entered as follows:

1. Item Stock Number.

2. Annual Volume (In Units) – this can be estimated, based on past experience.

3. Unit Cost.

The next step entails determination of the following for each inventory item:

4. Percent Of Number Of Items Stocked.

5. Annual Dollar Volume.

6. Percent Of Annual Dollar Volume.

The last step entails assigning a specific class to each group of inventories, i.e. Class A, Class B, or Class C.

ABC Inventory Analysis is not based on set of rigid requirements. On the contrary, the main objective of this flexible method is to help management to identify which inventories are really important (Class A), which are not so important (Class B), which are not really important (Class C), and invest the company’s limited financial resources accordingly.

Finally, ABC Inventory Analysis is designed to guide the operations management team in implementing strict Inventory Control measures for Class A, less restrictive for Class B, and least restrictive for Class C. This includes forecasting, purchasing, and physical control of inventories within the company. |

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

35. SMALL BUSINESS EXAMPLE

ABC INVENTORY ANALYSIS WORKSHEET |

|

|

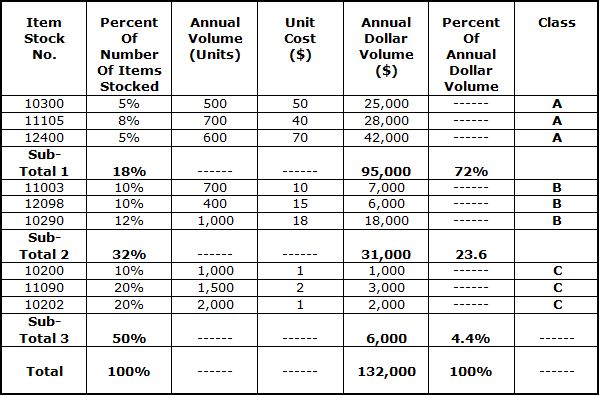

ABC INVENTORY ANALYSIS WORKSHEET APPLICATION |

Assume that XYZ Manufacturing Company has only 12 different items of inventory, which comprise its entire inventory requirements. The information about each item is entered into the ABC Inventory Analysis Worksheet as described below. |

ABC INVENTORY ANALYSIS WORKSHEET

|

|

|

|

36. CYCLE COUNTING |

|

|

CYCLE COUNTING |

Most business owners and operations managers know very well that there is always a discrepancy between the inventory records and the actual inventories values within every company. This is happening for several reasons, primarily because of the inventory recording errors and various inefficiencies caused by employees.

It is important, therefore, to conduct regular Inventory Audits designed to reconcile inventory records with the actual inventories on-hand. This process, also known as Inventory-Taking, usually causes an operational slow-down, since the entire facility has to be shut down during this process to ensure accurate results.

One of the practical methods designed to avoid a complete shut-down of the operational facility, and at the same time to ensure a high level of accuracy related to inventory records is called Cycle Counting. This method entails periodic counts and verification of inventory records for various items used by the operations department. Using the cycle counting procedure, management has constant access to updated inventory records.

The cycle counting method is based on ABC Inventory Analysis discussed earlier. All items of inventory must be classified as Class A, Class B or Class C items by specially trained employees. The company’s operations manager must determine the frequency of the cycle counting procedure for each class of inventories and instruct these employees to take count of various inventory items and enter this information into a Cycle Counting Worksheet accordingly.

A typical cycle counting may be based on the following guidelines:

• 1 month frequency for all Class A inventory items.

• 3 month frequency for all Class B inventory items.

• 6 month frequency for all Class C inventory items.

This is illustrated in the example below. |

ADVANTAGES OF CYCLE COUNTING |

1. |

Eliminates the need for annual inventory-taking procedures. |

2. |

Avoids the necessity of shutting down the entire operational facility. |

3. |

Eliminates the annual inventory adjustments surprises. |

4. |

Allows trained employees to audit the accuracy of inventory on regular basis. |

5. |

Helps to identify the inventory shortages and errors in the shortest possible time. |

6. |

Allows the maintenance of the most accurate inventory records. |

7. |

Allows taking immediate action in case of inventory mismanagement. |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

37. SMALL BUSINESS EXAMPLE

CYCLE COUNTING WORKSHEET |

|

|

CYCLE COUNTING IMPLEMENTATION |

Assume that XYZ Company has:

• 50 Class A inventory items with required cycle count frequency of 1 month.

• 100 Class B inventory items with required cycle count frequency of 3 month.

• 200 Class C inventory items with required cycle count frequency of 6 month.

All these items must be counted in accordance with the Cycle Count Frequency prescribed by the operations manager and information must be entered into the Cycle Counting Worksheet accordingly. The operations manager will assign the following number of specially trained employees for each Class of inventory as follows:

• Class A – 1 employee.

• Class B – 2 employees.

• Class C – 4 employees.

Each employee will be responsible to complete the cycle counting of inventory during the prescribed period by spreading the task on a daily basis to avoid backlog. |

CYCLE COUNTING WORKSHEET 1 |

Inventory Class: A |

Cycle Count Frequency: 1 Month |

Item

Stock

No. |

Inventory Quantity |

Inventory Value |

On

Record |

Actual

Count |

Variance |

Unit

Cost ($) |

Shortage

Cost ($) |

| |

|

|

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

|

| |

CYCLE COUNTING WORKSHEET 2 |

Inventory Class: B |

Cycle Count Frequency: 3 Month |

Item

Stock

No. |

Inventory Quantity |

Inventory Value |

On

Record |

Actual

Count |

Variance |

Unit

Cost ($) |

Shortage

Cost ($) |

| |

|

|

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

|

| |

CYCLE COUNTING WORKSHEET 3 |

Inventory Class: C |

Cycle Count Frequency: 6 Month |

Item

Stock

No. |

Inventory Quantity |

Inventory Value |

On

Record |

Actual

Count |

Variance |

Unit

Cost ($) |

Shortage

Cost ($) |

| |

|

|

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

38. MATERIAL STORAGE TYPES |

|

|

MATERIAL STORAGE |

When the delivery of inventories takes place, all items must be inspected and placed within the company's stores to ensure their safekeeping. Hence, Material Storage also represents an integral part of the material management and control system.

The types of Stores maintained by the company usually depend upon the manufacturing or operational requirements and may be classified into several types illustrated below. |

MATERIAL STORAGE TYPES |

|

|

|

|

|

|

|

Raw

Materials

Stores |

|

Components Or

Work-In-Process

Stores |

|

Finished

Goods

Stores |

|

Consumables

Stores |

|

|

STORES LAYOUT AND LOCATION |

Stores Layout And Location depends upon the individual needs and the size of the organization. The variation of requirements results from differences in facilities, specific arrangement of manufacturing, finishing, and assembly processes, and the nature of the manufacturing operation.

Type, size, and quantity of materials also play an important role in the layout of stores. However, some of the common principles applied to the process of locating stores are outlined below. |

PRINCIPLES OF LOCATING STORES |

1. |

Stores should be created to provide maximum space at a minimum cost. |

2. |

Stores should be located to meet the requirements of the manufacturing processes. |

3. |

Stores should provide for maximum flexibility to accommodate changing conditions. |

4. |

Stores should facilitate effective material handling procedures. |

|

|

|

39. MATERIAL STORAGE LOCATION OPTIONS |

|

|

MATERIAL STORAGE LOCATION OPTIONS |

Stores may be located on a centralized or decentralized basis, and each type of location has certain advantages and disadvantages.

The advantages of the Centralized Storing Facilities, which represent the traditional management approach, are outlined below.

The Decentralized Storing Facilities, on the other hand, prescribed by world class operational guidelines, such as Just-In-Time Methodology, also offer substantial advantages outlined below. |

ADVANTAGES OF CENTRALIZED STORING FACILITIES |

1. |

Improved supervision in the stores. |

2. |

Improved control over inventories. |

3. |

Improved stores service efficiency. |

4. |

Improved accuracy of the inventory counting procedures. |

5. |

Reduced space requirements. |

6. |

Reduced requirements of employees. |

|

| |

ADVANTAGES OF DECENTRALIZED STORING FACILITIES |

1. |

Reduced distances between inventories and the work stations. |

2. |

Reduced material travel time within the manufacturing facility. |

3. |

Reduced labor time spent on moving inventory to relevant work stations. |

4. |

Reduced machine set-up time. |

5. |

Reduced overall operations time. |

6. |

Increased overall productivity in the manufacturing facility. |

7. |

Reduced operations costs. |

8. |

Reduced number of non-value added activities. |

9. |

Reduced waste of time in the operations department. |

|

|

|

40. DUTIES OF A STOREKEEPER |

|

|

THE STOREKEEPER |

The storage and control of inventory plays an important role within the organization. This function is carried out by one or several Storekeepers depending upon the size and specific requirements of the company.

The usual Duties Of The Storekeeper cover a wide range of activities outlined below. |

DUTIES OF THE STOREKEEPER |

1. |

To receive and record all deliveries. |

2. |

To unpack goods and check the quantities and the quality against the relevant purchase order. |

3. |

To return defective goods and to prepare supporting documentation. |

4. |

To inform the buyer and the purchase originator of the receipt of goods. |

5. |

To arrange proper storage of raw materials, components, work-in-process, finished goods, consumables, and tools. |

6. |

To issue goods against authorized material, stores, or tool requisition. |

7. |

To maintain updated inventory control records. |

8. |

To arrange the dispatch of finished goods to customers. |

9. |

To count inventory of all materials placed in the stores. |

|

|

|

41. MATERIAL DISPATCH |

|

|

MATERIAL DISPATCH |

Another important task of operations management is to ensure timely delivery of products to customers. In order to facilitate economical and prompt delivery, it is necessary to develop and maintain effective Material Dispatch procedures.

The material dispatch function is usually carried out by the Dispatch Supervisor, but if the company's size does not justify a separate position, it may be performed by the Store's Supervisor.

The dispatch of finished products to various customers necessitates effective coordination of all activities related to material management procedures. Some of the important requirements of the material dispatch are outlined below. |

MATERIAL DISPATCH REQUIREMENTS |

1. |

Availability of all materials and components required for the manufacture and assembly of finished products prior to their dispatch. |

2. |

Timely assembly of finished products in accordance with a pre-determined production schedule and preparation for their dispatch. |

3. |

Availability of packaging materials. |

4. |

Availability of sufficient storage facilities. |

5. |

Availability of transport facilities. |

|

|

|

42. TRANSPORT CONTROL |

|

|

TRANSPORT CONTROL |

It is necessary to plan all deliveries in advance in order to reduce the delivery costs and to increase the efficiency of transport facilities.

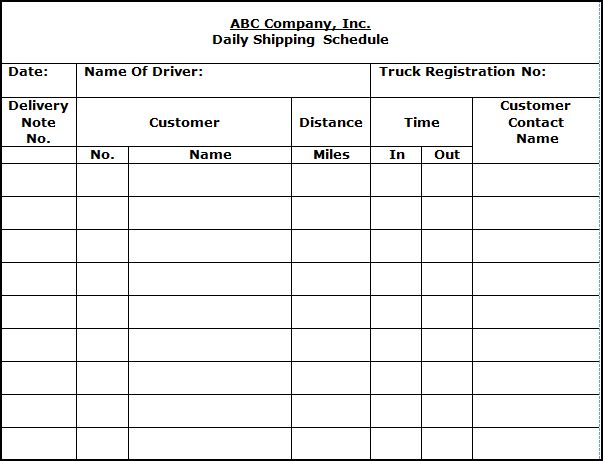

The nature of the Transport Control System usually depends upon the number of commercial vehicles utilized by the company. Some of the essential requirements of effective transport control facilities are outlined below.

An integral element of the materials dispatch procedure is preparation of a Daily Shipping Schedule. The prime purpose of this schedule is to summarize details of daily deliveries and to maintain control in the dispatch section. A typical Daily Shipping Schedule is presented below. |

THE TRANSPORT CONTROL REQUIREMENTS |

1. |

Daily delivery routing schedule. |

2. |

Restricted loading of vehicles. |

3. |

Skilled drivers. |

4. |

Constant control of the drivers' performance. |

5. |

Regular servicing and maintenance of vehicles. |

6. |

Monthly vehicle performance control. |

7. |

Monthly vehicle maintenance and repair cost control. |

|

|

|

43. SMALL BUSINESS EXAMPLE

DAILY SHIPPING SCHEDULE |

|

|

DAILY SHIPPING SCHEDULE |

|

|

|

44. FOR SERIOUS BUSINESS OWNERS ONLY |

|

|

ARE YOU SERIOUS ABOUT YOUR BUSINESS TODAY? |

Reprinted with permission. |

|

45. THE LATEST INFORMATION ONLINE |

|

|

| |

LESSON FOR TODAY:

Effective Supply Chain And Material Management Is

Of Material Importance To Your Company's Success!

|

Go To The Next Open Check Point In This Promotion Program Online. |

| |

|