MARKETING AND SALES MANAGEMENT

CHECK POINT 94: SALES PLANNING AND BUDGETING

Please Select Any Topic In Check Point 94 Below And Click. |

| |

| |

|

DO I NEED TO KNOW THIS CHECK POINT?

|

| |

WELCOME TO CHECK POINT 94 |

|

| |

HOW CAN YOU BENEFIT FROM CHECK POINT 94? |

| |

| The main purpose of this check point is to provide you and your management team with detailed information about Sales Planning And Budgeting and how to apply this information to maximize your company's performance. |

| |

| In this check point you will learn: |

| |

• About the basic steps in the sales planning and budgeting process.

• About key concepts in market measurement and forecasting.

• About three methods for determining sales potential.

• About sales forecasting factors and methods.

• About sales force composite opinion method.

• How to prepare detailed and summarized sales forecasts.

• About jury of executive opinion factors and a survey of buying intentions.

• About development of sales strategies.

• About evaluation of the sales force requirements.

• About the steps in the sales budgeting process... and much more. |

| |

LEAN MANAGEMENT GUIDELINES FOR CHECK POINT 94 |

| |

| You and your management team should become familiar with the basic Lean Management principles, guidelines, and tools provided in this program and apply them appropriately to the content of this check point. |

| |

| You and your team should adhere to basic lean management guidelines on a continuous basis: |

| |

| • |

Treat your customers as the most important part of your business. |

| • |

Provide your customers with the best possible value of products and services. |

| • |

Meet your customers' requirements with a positive energy on a timely basis. |

| • |

Provide your customers with consistent and reliable after-sales service. |

| • |

Treat your customers, employees, suppliers, and business associates with genuine respect. |

| • |

Identify your company's operational weaknesses, non-value-added activities, and waste. |

| • |

Implement the process of continuous improvements on organization-wide basis. |

| • |

Eliminate or minimize your company's non-value-added activities and waste. |

| • |

Streamline your company's operational processes and maximize overall flow efficiency. |

| • |

Reduce your company's operational costs in all areas of business activities. |

| • |

Maximize the quality at the source of all operational processes and activities. |

| • |

Ensure regular evaluation of your employees' performance and required level of knowledge.

|

| • |

Implement fair compensation of your employees based on their overall performance.

|

| • |

Motivate your partners and employees to adhere to high ethical standards of behavior. |

| • |

Maximize safety for your customers, employees, suppliers, and business associates. |

| • |

Provide opportunities for a continuous professional growth of partners and employees. |

| • |

Pay attention to "how" positive results are achieved and constantly try to improve them. |

| • |

Cultivate long-term relationships with your customers, suppliers, employees, and business associates. |

|

|

|

1. THE SALES PLANNING AND BUDGETING PROCESS |

|

|

THE SALES PLANNING AND BUDGETING PROCESS |

Business owners and sales managers must remember that sales planning and budgeting is one of the key sales management functions in every business organization.

The first important function of the sales manager is to initiate the Sales Planning And Budgeting Process. This process should be implemented by the sales manager in accordance with realistic estimates of the sales volume likely to be achieved during the forthcoming fiscal period.

The sales planning and budgeting process normally entails three steps outlined below. |

STEPS IN THE SALES PLANNING AND BUDGETING PROCESS

Step 1: Appropriate Market Analysis.

Identify market segments where your company is planning to do business.

Step 2: Measurement Of Sales Potential.

Estimate the sales potential of each market segment in accordance with marketing intelligence information at your disposal.

Step 3: Sales Forecasting.

Develop sales forecasts based on realistic expectations in accordance with the existing conditions in the marketplace and your company's internal abilities. |

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

|

2. SALES POTENTIAL |

|

|

SALES POTENTIAL IS A PART OF MARKET MEASUREMENT AND FORECSATING

The process of estimating Sales Potential for various products and services has been described in detail in this Tutorial. This process represents a part of the market measurement and forecasting procedure, and it is illustrated below. |

KEY CONCEPTS IN MARKET MEASUREMENT AND FORECASTING |

| |

|

| |

SALES POTENTIAL

There are several methods for determining sales potential for products or services in the specific market. Some of these methods for assessing the Current Market Demand and Sales Potential are explained in detail in Tutorial 5.

Evaluation of the company's sales potential in selected market segments helps management in preparing more accurate sales forecasts. Three of these methods are mentioned below. |

THREE METHODS FOR DETERMINING SALES POTENTIAL

|

|

|

|

|

The

Chain-Ratio

Method |

|

The

Market-Buildup

Method |

|

The

Buying-Power-Index

Method |

| |

|

|

|

3. SALES FORECAST |

|

|

SALES FORECASTS

Sales Forecast provides a quantitative estimate of the level of actual sales, expressed in monetary terms, or of units of product to be sold during a specified period of time. The sales forecast is usually prepared on an annual basis, taking into consideration several factors illustrated below. |

SALES FORECASTING FACTORS

|

|

|

|

|

|

|

Past

Sales

Performance |

|

Existing

Market

Conditions |

|

Product

Demand

Fluctuations |

|

Competition |

|

|

| |

IMPORTANCE OF SALES FORECASTS

Sales Forecast provides an important foundation for the financial, production, and human resources departments to plan their work and ascertain their needs for the forthcoming budgeted period. Managers, however, must be careful in using the sales forecast estimates for two reasons outlined below. |

WHY SHOULD MANAGERS BE CAREFUL WITH SALES FORECASTS? |

1. |

If the sales forecast is too optimistic, the company can sustain substantial losses as a result of an over-expenditure of funds in anticipation of an income level that has not been achieved. |

2. |

If the sales forecast is too low, the company may not be in a position to accommodate all market needs and may subsequently forgo profits and present its competitors with additional sales opportunities. |

|

There are several Sales Forecasting Methods commonly used by managers in preparing sales forecasts. Three of these methods are illustrated below. |

SALES FORECASTING METHODS

|

|

|

|

|

Sales Force

Composite

Opinion |

|

Jury Of

Executive

Opinion |

|

Survey Of

Buying

Intentions |

|

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

4. SALES FORCE COMPOSITE OPINION |

|

|

SALES FORCE COMPOSITE OPINION

Sales Force Composite Opinion is a popular sales forecasting method frequently used by sales managers.

In accordance with this method, each sales person is required to prepare Individual Sales Projections for the forthcoming fiscal year and to submit a detailed sales forecast to the sales manager. These projections, illustrated in the Detailed Sales Forecast below, must be based on realistic sales estimates, taking into consideration past results and future expectations. Subsequently, all sales projections must be added up in a Summarized Sales Forecast to obtain the final forecast of sales volume as illustrated below.

Active participation by each member of the sales team and preparation of the sales forecast by customer, product, and sales territory represent the major advantages of this method. |

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

|

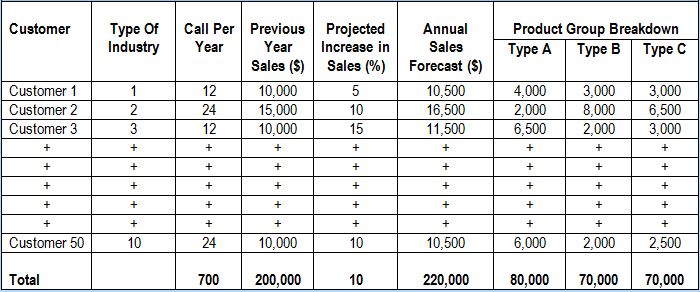

5. SMALL BUSINESS EXAMPLE

DETAILED SALES FORECAST |

|

|

DETAILED SALES FORECAST |

ABC Company, Inc.

Detailed Sales Forecast

Period: January 2014 - December 2014

|

|

|

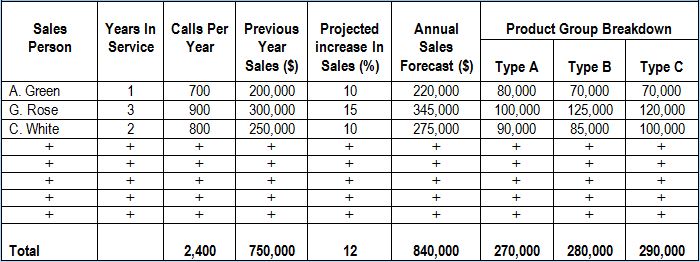

6. SMALL BUSINESS EXAMPLE

SUMMARIZED SALES FORECAST |

|

|

SUMMARIZED SALES FORECAST |

ABC Company, Inc.

Summarized Sales Forecast

Period: January 2014 - December 2014

|

|

|

7. JURY OF EXECUTIVE OPINION |

|

|

JURY OF EXECUTIVE OPINION

Jury Of Executive Opinion is another forecasting method commonly used by sales managers. This method is based on Sales Forecasts prepared by several members of the company's management team. All participating executives prepare an individual sales forecast using their own judgment. Subsequently, all individual sales projections are evaluated and finally added up.

Active participation by the company's executives has proven to be useful in preparing accurate short-term forecasts. This method, however, demands substantial experience and understanding of overall requirements in the marketplace. Several factors that are usually considered during the Jury Of Executive Opinion procedure are outlined below. |

JURY OF EXECUTIVE OPINION FACTORS

|

|

|

|

|

|

|

Nature Of

Company's

Products

Or Services |

|

Customers'

Requirements |

|

Competition |

|

Economic

Conditions In

The Marketplace |

| |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

8. SURVEY OF BUYING INTENTIONS |

|

|

SURVEY OF BUYING INTENTIONS

A Survey Of Buying Intentions can be used as an alternative or an addition to the above mentioned sales forecasting methods. This method entails surveying a sample of customers to determine the types and quantities of products or services they are likely to buy in the future.

A survey of buying intentions may be conducted by using a broad range of communication media illustrated below. |

COMMUNICATION MEDIA USED IN A SURVEY OF BUYING INTENTIONS

|

|

|

|

|

|

|

Personal

Interviews |

|

Phone |

|

Mail

Questionnaires |

|

Internet |

|

|

| |

IMPORTANCE OF USING SEVERAL SALES FORECASTING METHODS

In a Survey Of Buying Intentions, all customer responses are subsequently evaluated and added up to determine the total demand for each product.

This method has proven to be useful in preparing sales forecasts for industrial goods in well-defined small market segments. However, it is often a time consuming and expensive method that does not guarantee that interviewed customers will always act according to their original answers and intentions.

Since most organizations offer a variety of products or services to different customers in a constantly changing market environment, it is often impractical to use only one sales forecasting method. For this reason, sales managers often use a combination of methods and utilize the input from sales people, executive managers, and customers at the same time. |

ADDITIONAL INFORMATION ONLINE |

|

|

|

9. SALES STRATEGIES |

|

|

SALES STRATEGIES

Once Sales Forecasts are prepared and overall Sales Objectives are established, it is necessary to develop a detailed Sales Plan which will provide guidance to the company's management in the process of achieving their objectives.

A well-defined plan must be based on a set of appropriate Sales Strategies for the forthcoming fiscal year. These strategies represent the continuation of the Marketing Strategies which are discussed in detail in Tutorial 5. Some examples of sales strategies that could be adopted by a sales manager are outlined below. |

DEVELOPMENT OF SALES STRATEGIES |

Marketing Strategies

|

|

|

|

|

New Venture

Strategy |

Growth

Strategy |

Market

Development

Strategy |

Market

Retention

Strategy |

Balancing

Strategy |

|

|

|

|

|

Develop A Set Of Appropriate Sales Strategies

|

|

|

|

|

Sell New

Products Or

Services To

Existing

Customers |

Offer More

Attractive Discounts To Existing Customers |

Offer

Improved

Products Or

Services At

Reduced

Prices |

Reduce

Product Or

Service Range

And Increase

The Sales

Volume |

Sell Existing

Products Or

Services And

Maintain The

Sales Volume |

|

|

|

|

|

Reduce Price Of Existing Products Or Services And Offer These To Current And Potential Customers |

Offer Excess Inventory To Customers At Reduced Prices |

|

|

|

|

|

Demonstrate

The Advantages

Of New Products

Or Services |

Introduce

New Sales

Promotion

Methods |

Develop

New Accounts

And Eliminate

Unprofitable

Accounts |

Reduce

Marketing

And Sales

Overheads |

Eliminate

Unprofitable

Product Or

Service Lines |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

10. EVALUATION OF THE SALES FORCE REQUIREMENTS |

|

|

THE SALES FORCE REQUIREMENTS

The next step in the sales planning effort entails Evaluation Of Sales Force Requirements to meet the company’s sales objectives. The sales manager must assess the overall sales plan, evaluate each of the three options presented below, and select the most appropriate option. |

THREE OPTIONS IN THE SALES FORCE REQUIREMENTS

|

|

|

|

|

Reduce

The Sales Force |

|

Maintain

The Sales Force |

|

Increase

The Sales Force |

| Reduce the present number of sales people. |

|

Maintain the present number of sales people. |

|

Increase the present number of sales people. |

| |

|

If the number of sales people must be increased, the sales manager must make a choice between two options outlined below. |

TWO OPTIONS FOR INCREASING THE SALES FORCE

1. |

To use outside agents. |

2. |

To hire new sales people. |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

11. ADVANTAGES AND DISADVANTAGES OF USING OUTSIDE SALES AGENTS |

|

|

SALES AGENTS OR INDEPENDENT REPRESENTATIVES

One of the options available to business owners and sales managers is to employ outside Sales Agents or Independent Sales Representatives (Sales Reps) to sell the company’s products and services in the marketplace. The use of agents or independent representatives has several advantages outlined below. |

ADVANTAGES OF USING OUTSIDE SALES AGENTS |

1. |

Sales agents already have a network of well-established contacts. |

2. |

Sales agents usually have good experience in their product lines and maintain high standards of work. |

3. |

Sales agents do not incur administrative costs for a company. |

4. |

Sales agents get paid only if they are successful in selling the company’s products or services. |

|

| |

DISADVANTAGES OF USING OUTSIDE SALES AGENTS

One of the prime disadvantages in dealing with sales agents is that their activities cannot always be effectively controlled by the sales manager. This may present a particular problem since sales agents plan their own movements in the marketplace and work according to their own time schedules. |

|

|

12. ADVANTAGES AND DISADVANTAGES OF USING SALES PEOPLE |

|

|

SALES PEOPLE

Another option that can be exercised by the business owner and the sales manager is to hire Sales People. This option may also present certain advantages and disadvantages which are summarized below. |

ADVANTAGES OF USING SALES PEOPLE |

1. |

Sales people can be trained according to the company's specific requirements. |

2. |

Sales people can be allocated to defined sales territories, customers, and product or service lines. |

3. |

The performance of sales people can be planned as a part of the overall sales effort. |

4. |

The performance of sales people can be monitored and controlled on a regular basis. |

|

| |

COST OF USING SALES PEOPLE

The employment of sales people may represent a costly exercise. It is essential, therefore, to assess the need for additional sales employees and to estimate the total cost of their employment. Estimating the Sales Force size entails a number of considerations and may be carried out in several ways.

Two Methods For Estimating The Sales Force Requirements commonly used by business owners and sales managers are illustrated below. |

METHODS FOR ESTIMATING THE SALES FORCE REQUIREMENTS

|

|

|

The "How Much Can

The Company Afford" Method |

|

The "Number

Of Sales Calls" Method |

| |

|

|

|

13. THE "HOW MUCH CAN THE COMPANY AFFORD" METHOD |

|

|

THE "HOW MUCH CAN THE COMPANY AFFORD" METHOD

The "How Much Can The Company Afford" Method is based on matching two basic variables outlined below. This method has an advantage since all sales costs will remain in line with the company's projected revenues. The main disadvantage, however, is that this method does not account for the real needs of customers in the marketplace. |

TWO VARIABLES OF THE

"HOW MUCH CAN THE COMPANY AFFORD" METHOD |

1. |

A number of sales people at a pre-determined average cost per employee. |

2. |

A specific sales budget allocation. |

|

|

|

14. SMALL BUSINESS EXAMPLE

THE "HOW MUCH CAN A COMPANY AFFORD" METHOD |

|

|

THE "HOW MUCH CAN A COMPANY AFFORD" METHOD

Consider, for example, a medium-sized company that:

| • |

Projects $10 million in sales for the forthcoming fiscal year. |

| • |

Allocates 5 percent of its revenue toward sales activities. |

Assume that:

| • |

Sales supervision requires 20 percent of the sales budget. |

| • |

The total cost of each sales person is $50,000 per year, including straight salary, commission, and travel allowance. |

Description |

Calculation |

Result |

Total Budgeted Revenue From Sales |

- |

$10,000,000 |

Total Sales Budget Allocation |

$100,000 x 0.05 |

$500,000 |

Total Cost Of Sales Supervision |

$500,00 x 0.2 |

$100,00 |

Total Cost Allocated

To The Sales Force |

$500,000 - $100,000 |

$ 400,000 |

Total Number Of Sales People |

At $50,000 Per Sales Person Per Year |

8 Sales People |

|

|

|

15. THE "NUMBER OF SALES CALLS" METHOD |

|

|

THE "NUMBER OF CALLS" METHOD

The "Number Of Sales Calls" Method, on the other hand, is designed to develop a sales force in accordance with specific customer needs. This method takes into account four variables outlined below. (47)

The size of the sales force can be determined as follows:

|

FOUR VARIABLES IN THE "NUMBER OF CALLS" METHOD |

1. |

The number of existing and potential customers. |

2. |

The average number of sales calls per year required by each customer. |

3. |

The length of each sales call. |

4. |

The selling time available per sales person. |

|

| |

FORMULA KEY: |

A |

Number of existing customers. |

B |

Number of potential customers. |

C |

Required sales call frequency. |

D |

Average length of a sales call. |

E |

Selling time available per sales person. |

|

| |

ADVANTAGES OF THE "NUMBER OF CALLS" METHOD

The "Number Of Sales Calls" Method enables the sales manager to determine the required size of the company's sales force well in advance in accordance with specific customer needs.

One of the drawbacks of this method, however, is its failure to account for income and expenditures associated with different aspects of customer service. Thus, it becomes difficult to establish whether the current frequency of sales calls enables the company to maximize its profits through servicing customers. |

|

|

16. SMALL BUSINESS EXAMPLE

THE "NUMBER OF SALES CALLS" METHOD |

|

|

THE "NUMBER OF SALES CALLS" METHOD

Consider, for example, a medium-sized company that:

| • |

Has 200 existing customers. |

| • |

Plans to open 50 additional new accounts. |

Assume that:

| • |

Each customer should ideally be called at least once every two months, or six times a year. |

| • |

Each sales call requires an average of two hours, including travel time. |

| • |

The selling time available per sales person is 1,500 hours per year. |

The size of the sales force can be determined as follows:

| Number Of Sales People = |

(200 + 50) x 6 x 2 |

= 2 Sales People |

| 1,500 |

In reality, however, the company's customers usually vary in size and subsequently will have different needs. These needs, in turn, should be translated into:

An ideal frequency of sales calls per year for each customer.

Consider, for example, that the company has:

| • |

40 large present and potential customers that require 18 calls per year. |

| • |

100 medium-sized customers that require 12 calls per year. |

| • |

110 small customers that require 3 calls per year. |

Assuming that the average length of each sales call and the selling time per sales person remain unchanged, the size of the sales force can be determined as follows:

| Number Of Sales People = |

[(40 x 18) + (100 x 12) + (110 x 3)] x2 |

= 3 Sales People |

| 1,500 |

|

|

|

17. ADVANTAGES OF HIRING EXPERIENCED SALES PEOPLE |

|

|

HIRING OF SALES PEOPLE

Once the size of the sales force is determined, it becomes necessary to decide between hiring experienced or inexperienced Sales People, as illustrated below. Thus, the final decision regarding the choice of suitable sales people remains with the business owner or the sales manager. |

TWO OPTIONS FOR HIRING SALES PEOPLE

|

|

|

Hiring Experienced

Sales People |

|

Hiring Inexperienced

Sales People |

| Hiring experienced sales people will enable the company to respond to immediate market demands and to provide better service to customers. However, the high compensation package often required by experienced sales people may be a deterrent. |

|

Hiring inexperienced sales people may be less costly in terms of the compensation package, but it will require additional investment in sales training. In the long run this may not be the most cost-effective option. |

|

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

18. SALES BUDGET |

|

|

SALES BUDGET

The ultimate task of the sales planning process is development of a sound Sales Budget. All components of the sales budget must be prepared on an annual basis and thereafter divided into monthly targets in accordance with relevant sales projections.

The sales budget summarizes all details related to several important elements outlined below. |

ELEMENTS OF A SALES BUDGET |

1. |

The projected level of the company’s sales throughout the budgeted period. |

2. |

The selling expenditure budget, including salaries and commissions of sales employees. |

3. |

The advertising budget. |

4. |

The sales administration budget. |

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

19. THE SALES BUDGETING PROCESS |

|

|

THE SALES BUDGETING PROCESS

The main purpose of the Sales Budgeting Process is to enable the management team to lead its organization toward a predetermined goal and to achieve the desired level of the company's profitability. A typical sales budgeting process entails a number of steps outlined below. |

STEPS IN THE SALES BUDGETING PROCESS

Step 1: Become Familiar With The Company's Marketing Plan.

Step 2: Formulate The Company's Sales Objectives In Accordance With The Company's Marketing Plan.

Step 3: Prepare Annual Sales Forecasts Per Product, Or Service, Or Customer, Or Sales Territory, Or A Combination Thereof.

Step 4: Identify Personal Selling And Promotional Requirements Needed To Meet The Company's Sales Objectives.

Step 5: Summarize Estimated Values Of Annual Sales Forecasts And Selling Costs And Prepare A Budget.

Step 6: Compare Actual Sales Revenues And Selling Costs With The Budgeted Values On A Monthly Basis And Identify Budget Variances.

Step 7: Evaluate All Budget Variances And Use Them For Controlling Purposes And For Further Budget Revisions (Refer back to Step 5). |

|

|

20. SALES BUDGETING FACTORS |

|

|

SALES BUDGETING

The Sales Budget must be prepared by the sales manager in accordance with realistic estimates of sales volume likely to be achieved during the forthcoming fiscal period.

Main factors that usually influence the Sales Budgeting Process, discussed in Tutorial 3, are outlined below. As a result of detailed evaluation of these factors, the sales manager is expected to prepare accurate sales budgets pertaining to all products or services offered by the company. |

SALES BUDGETING FACTORS |

1. |

Nature of the company's products and services. |

2. |

History of previous sales. |

3. |

Seasonal variations in product or service demand. |

4. |

The company's current position in the marketplace. |

5. |

Influence by competitors. |

6. |

The company's plans for new product or service development. |

7. |

Expected product or service demand in the marketplace. |

8. |

Economic stability in the marketplace. |

9. |

Rate of inflation. |

|

Sales budgets provide quantitative estimates of the level of sales, expressed in various terms, as illustrated below. |

TERMS OR UNITS USED IN THE SALES BUDGET

|

|

|

|

|

Monetary

Terms |

|

Units Of Product

To Be Sold |

|

Units Of Service

To Be Rendered |

| |

|

A simplified Sales Budget for a company is presented below. |

ADDITIONAL INFORMATION ONLINE |

|

|

|

21. SMALL BUSINESS EXAMPLE

SALES BUDGET |

|

|

SALES BUDGET

ABC Corporation

Sales Budget

Period: January 1, 2014 - December 31, 2014 |

Product Or Service

Description |

Estimated Value ($) |

Annual |

Monthly |

Product (Service) Type A |

900,000 |

75,000 |

Product (Service) Type B |

600,000 |

50,000 |

Product (Service) Type C |

300,000 |

25,000 |

Product (Service) Type D |

300,000 |

25,000 |

Total Projected Sales (Revenue) |

2,100,000 |

175,000 |

Sales Manager:

B. Blue |

President:

C. Gray |

Date:

December 20, 2013 |

|

|

|

|

22. FOR SERIOUS BUSINESS OWNERS ONLY |

|

|

ARE YOU SERIOUS ABOUT YOUR BUSINESS TODAY? |

Reprinted with permission. |

|

23. THE LATEST INFORMATION ONLINE |

|

|

| |

LESSON FOR TODAY:

If You Don't Know Where You Are Going -

You Might Wind Up Someplace Else!

Yogi Berra

|

| |

|